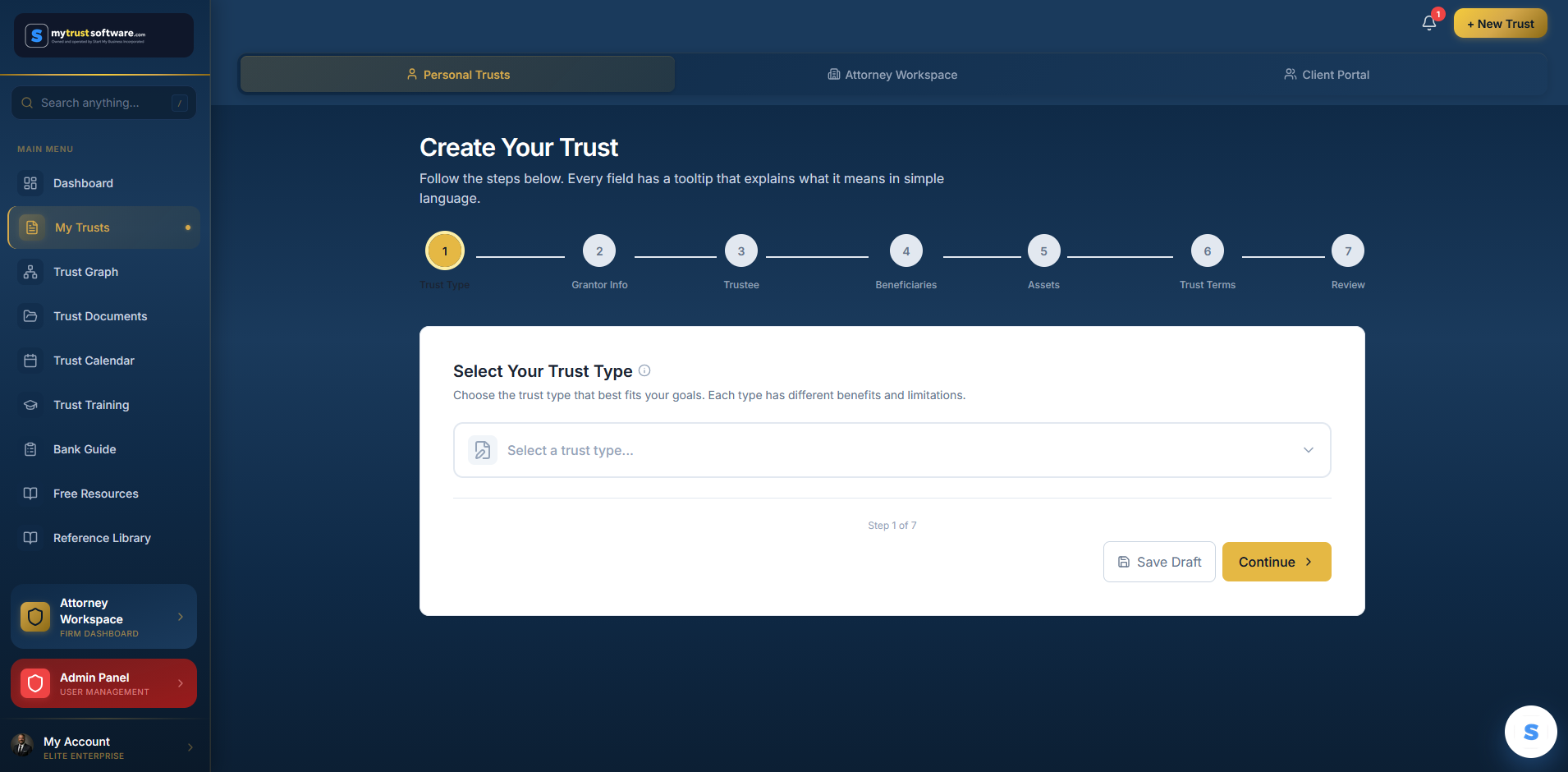

What Exactly Is a Trust, and Why Does Your Family Need One?

A trust is not just for the wealthy. It is a basic tool that protects every family.

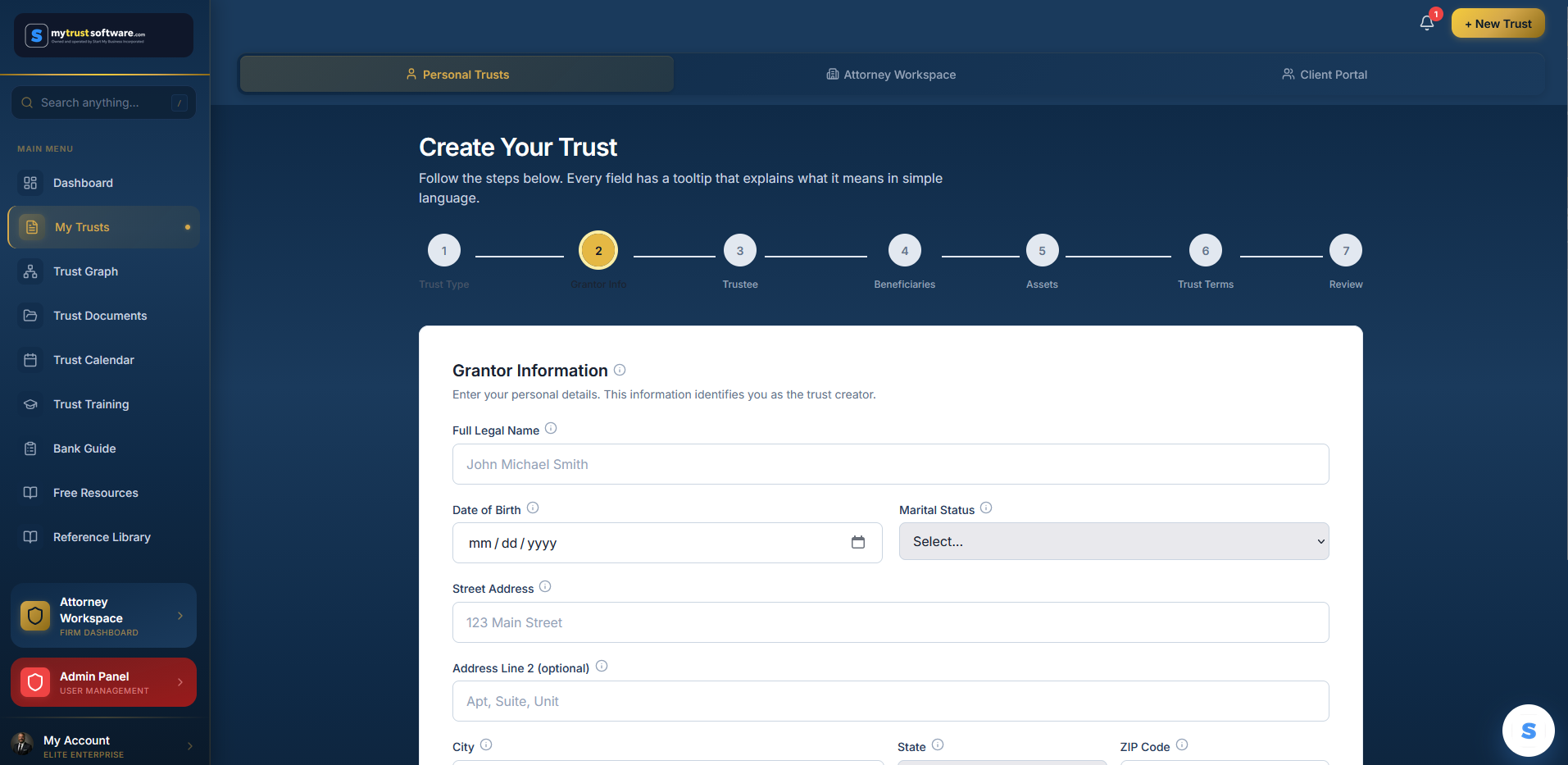

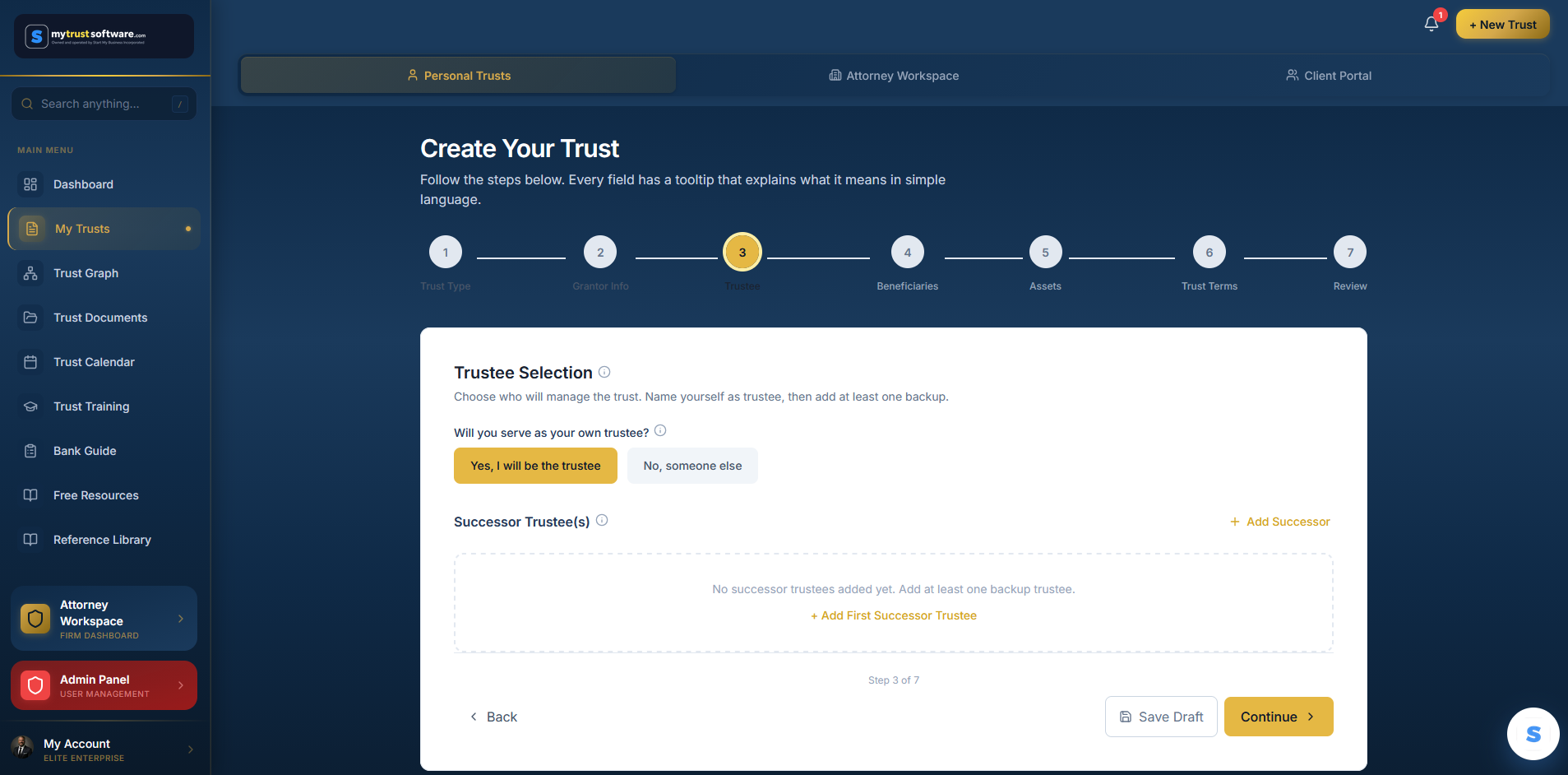

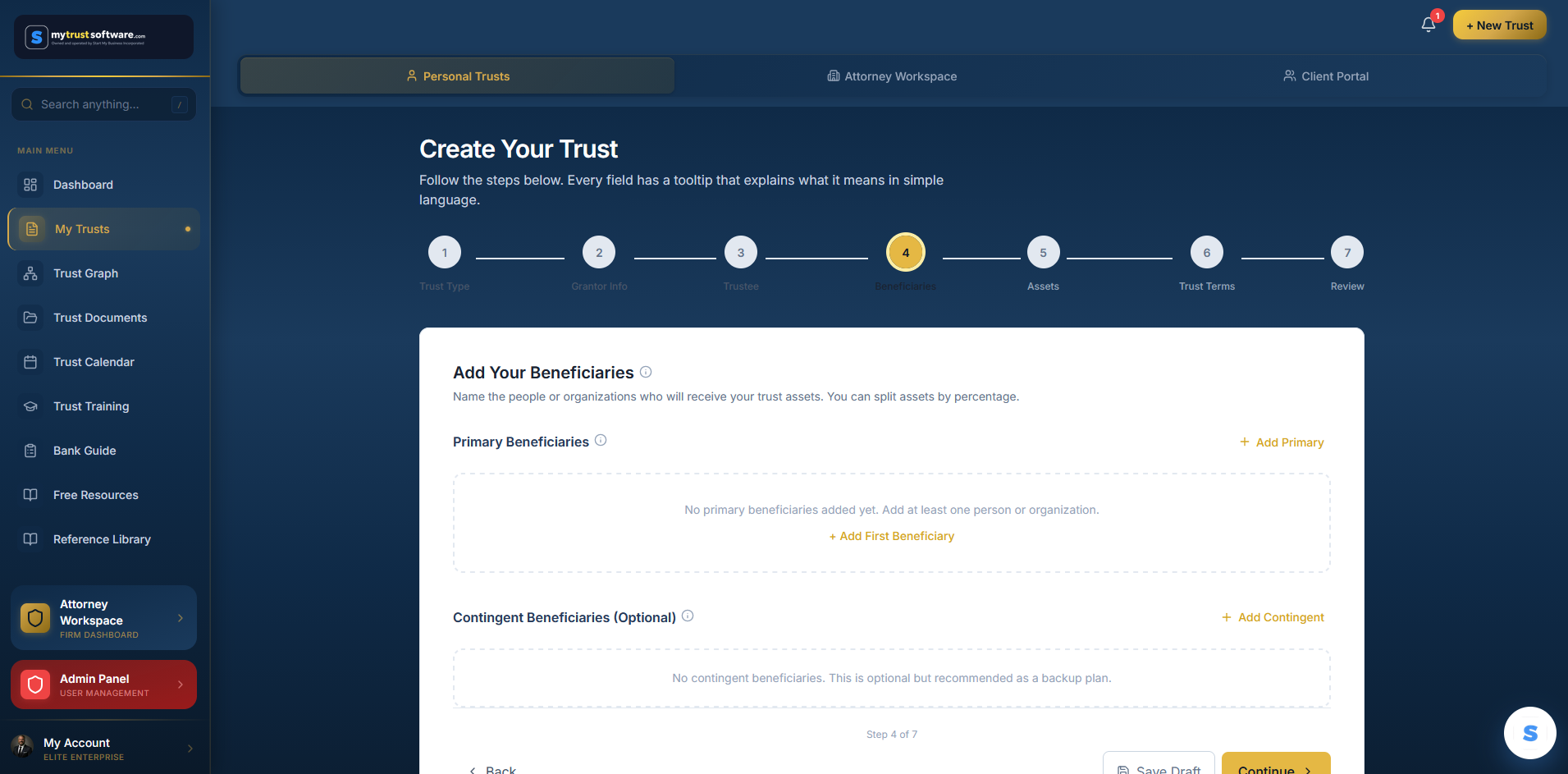

A trust is just a document that names three roles: who owns the assets, who manages them, and who receives them. Here is how those parties relate.

Grantor

Creates the trust and places assets in it

Trustee

Manages assets per the instructions

Successor Trustee

Steps in at incapacity or death

Beneficiaries

Receive assets on your terms

Key Takeaways

Trusts skip probate, saving your family 3-7% of your estate value

Your estate stays completely private (probate is public record)

A trust protects you during your lifetime if you become incapacitated

Parents can control when and how children receive their inheritance

You do not need to be wealthy to benefit from a trust

Most people hear the word "trust" and think of wealthy families with teams of lawyers. That picture is outdated and wrong. A trust is simply a legal document that says: here are my assets, here is who manages them, and here is who gets them when I am gone.